Simply Statistics

Universities Do Spend Indirect Costs on Research, And It’s Still Not Enough

Many, including prominent scientists, seem to misunderstand the true cost of biomedical research and the fact that universities subsidize it beyond what they receive from the NIH.

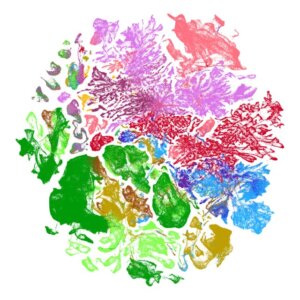

Biologists, stop putting UMAP plots in your papers

UMAP is a powerful tool for exploratory data analysis, but without a clear understanding of how it works, it can easily lead to confusion and misinterpretation.

Russell Shinohara is awarded the 2023 Mortimer Spiegelman Award

The analyst is a random variable

What is artificial intelligence? A three part definition

Is Code the Best Way to Represent a Data Analysis?

Code is a useful representation of a data analysis for the purposes of transparency and opennness. But code alone is often insufficient for evaluating the quality of a data analysis and for determining why certain outputs differ from what was expected. Is there a better way to represent a data analysis that helps to resolve some of these questions?

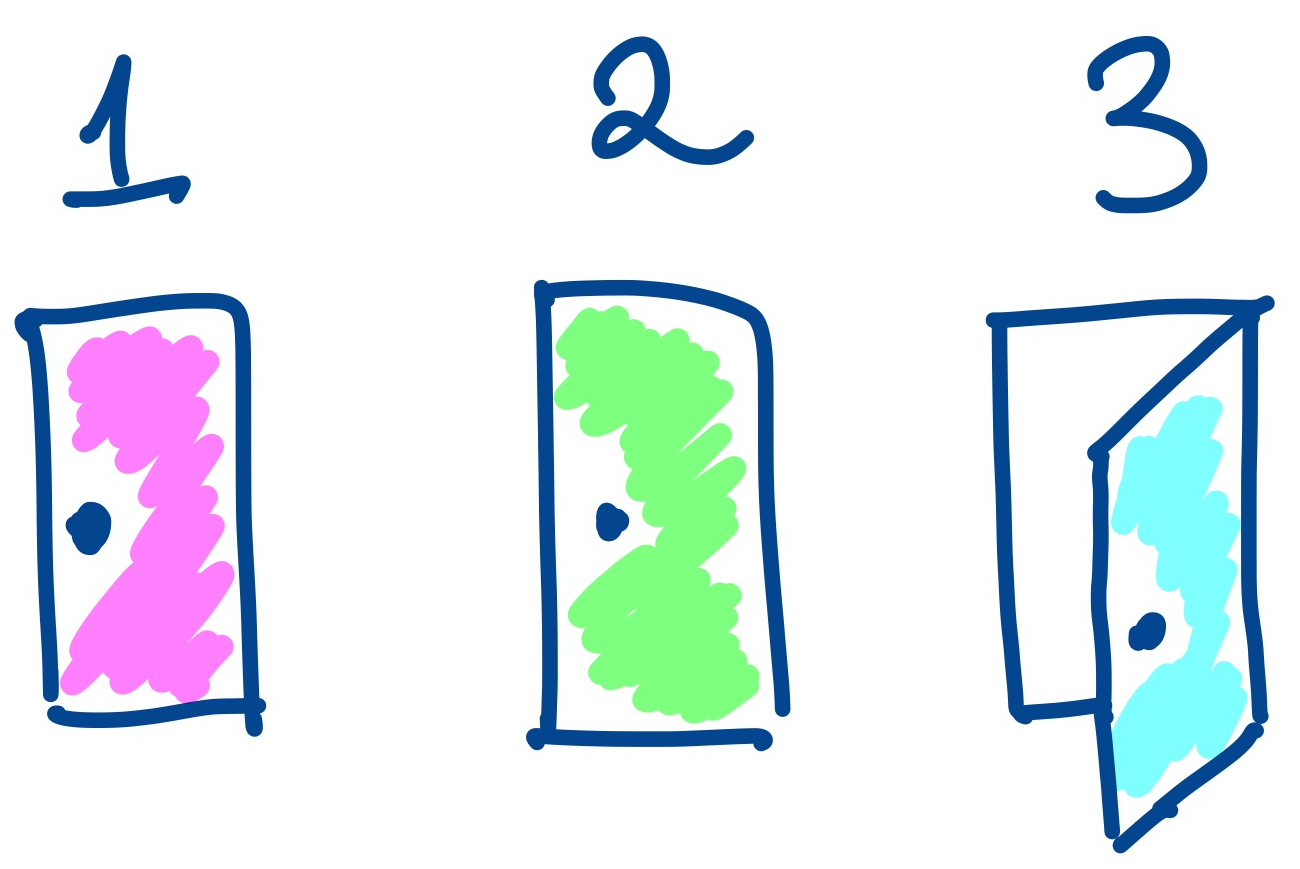

Narrative Failure in Data Analysis

A data analysis can fail if it doesn't present a coherent story and "close all the doors". Such a failure is not simply a problem with communication, but often indicates a problem with the details of the analysis itself.

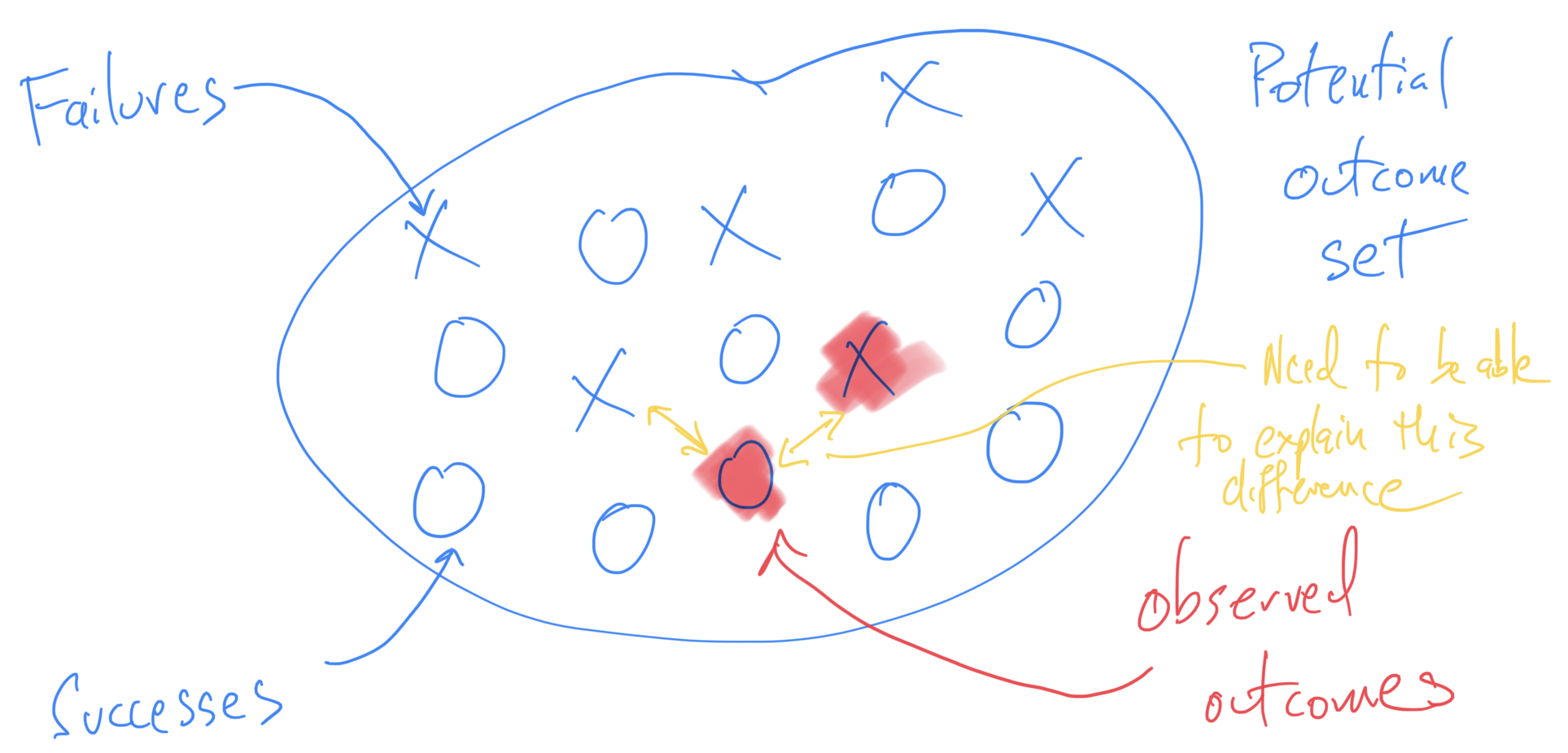

Thinking About Failure in Data Analysis

Streamline - tidy data as a service

The Four Jobs of the Data Scientist

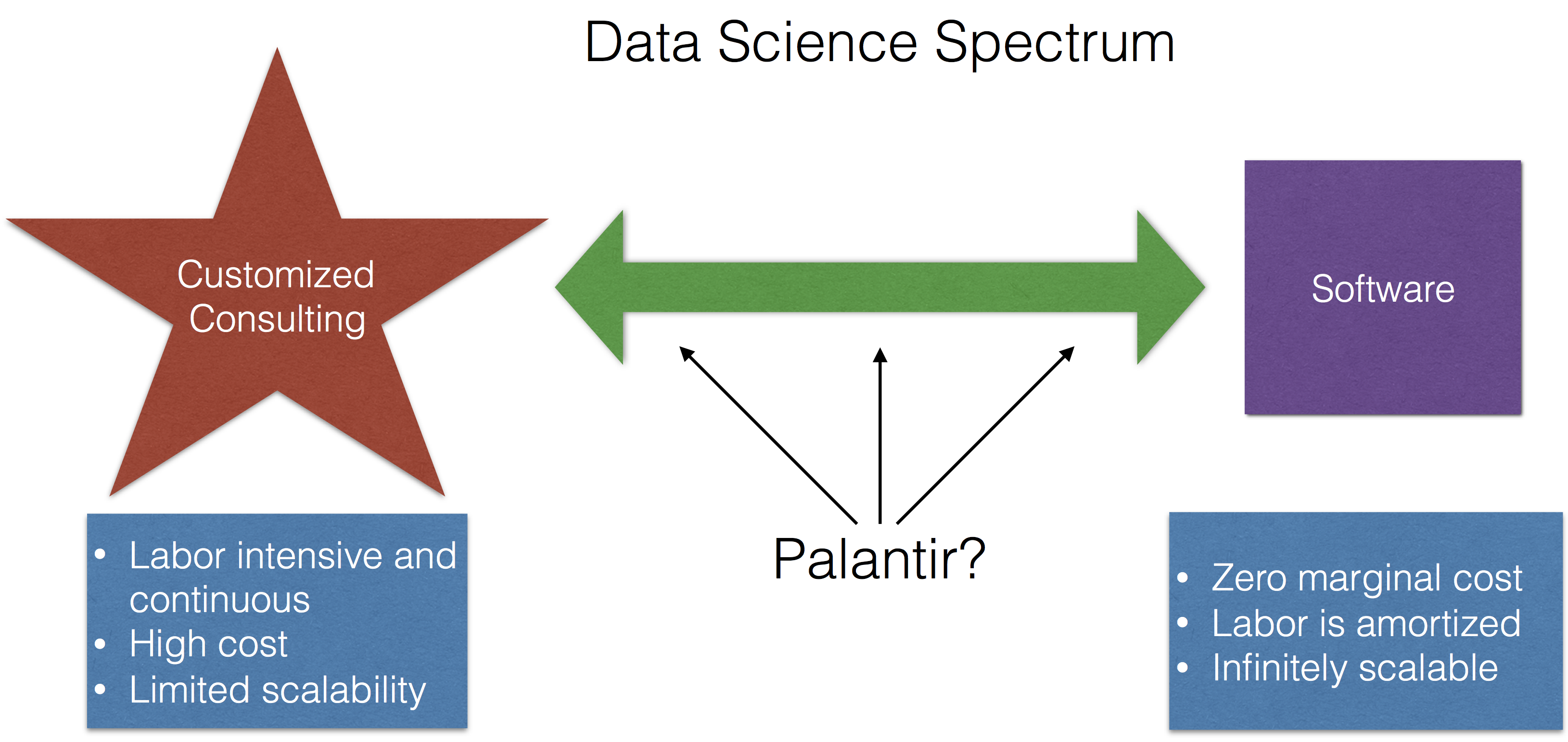

Palantir Shows Its Cards

Asymptotics of Reproducibility

Amplifying people I trust on COVID-19

Is Artificial Intelligence Revolutionizing Environmental Health?

You can replicate almost any plot with R

So You Want to Start a Podcast

The data deluge means no reasonable expectation of privacy - now what?

More datasets for teaching data science: The expanded dslabs package

Research quality data and research quality databases

I co-founded a company! Meet Problem Forward Data Science

Generative and Analytical Models for Data Analysis

Tukey, Design Thinking, and Better Questions

Interview with Abhi Datta

10 things R can do that might surprise you

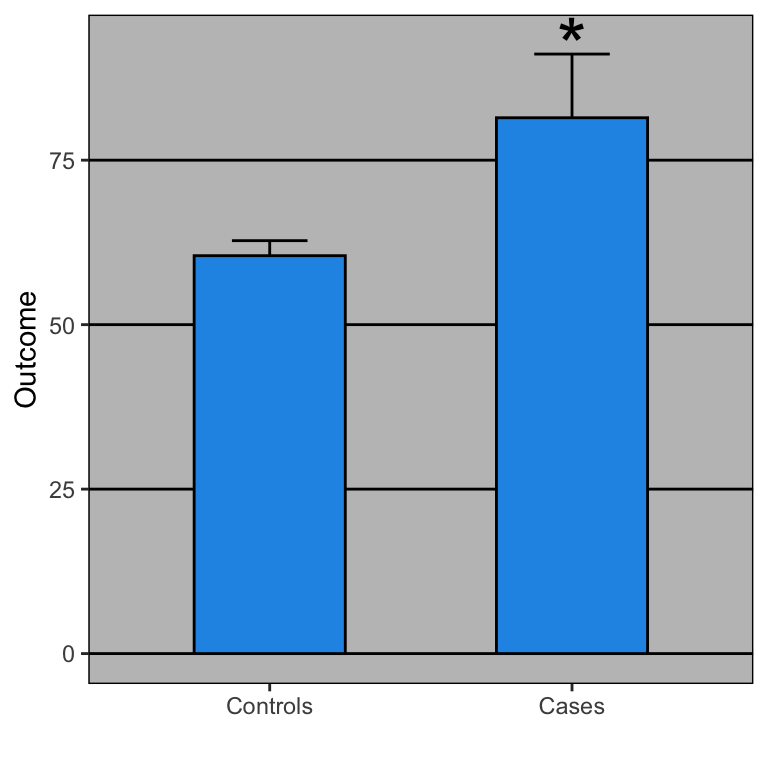

Open letter to journal editors: dynamite plots must die

Interview with Stephanie Hicks

The Tentpoles of Data Science

How Data Scientists Think - A Mini Case Study

The Netflix Data War

The Role of Theory in Data Analysis

The role of academia in data science education

Guest Post: Galin Jones on criteria for promotion and tenture in (bio)statistics departments

The economic consequences of MOOCs

Chromebook Data Science - a free online data science program for anyone with a web browser.

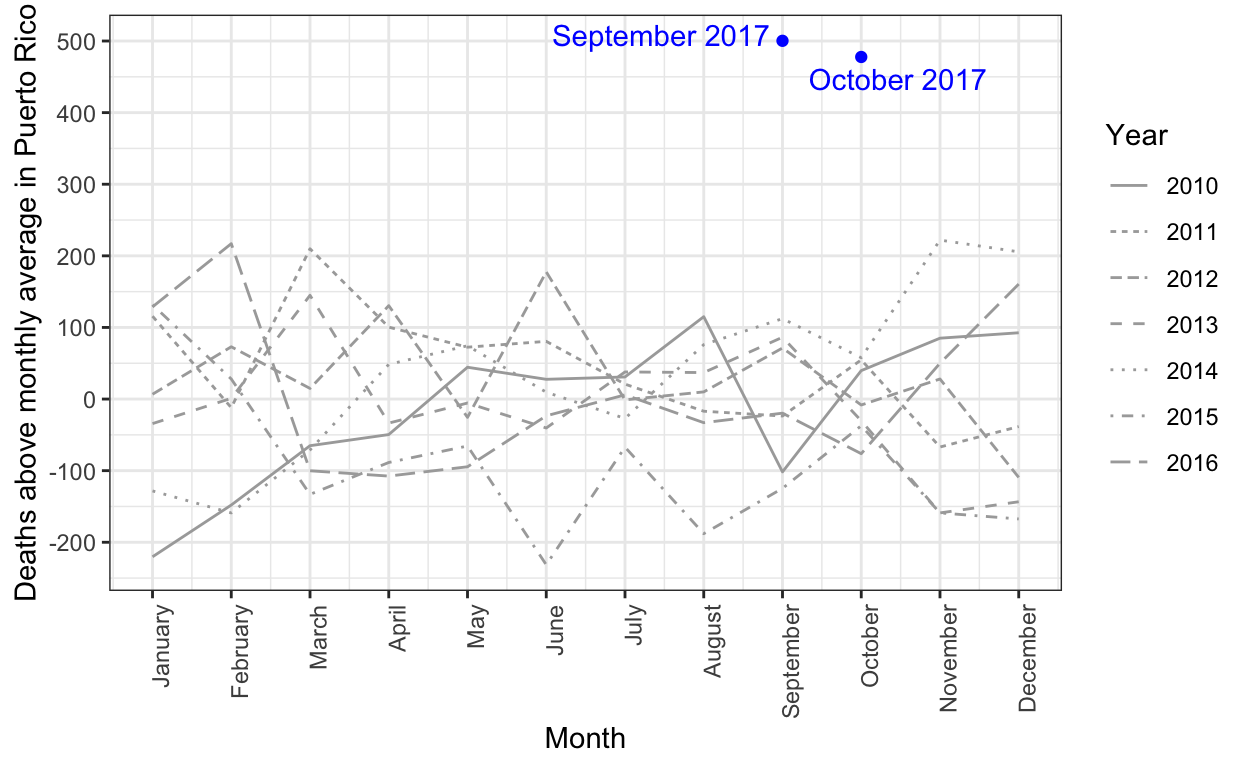

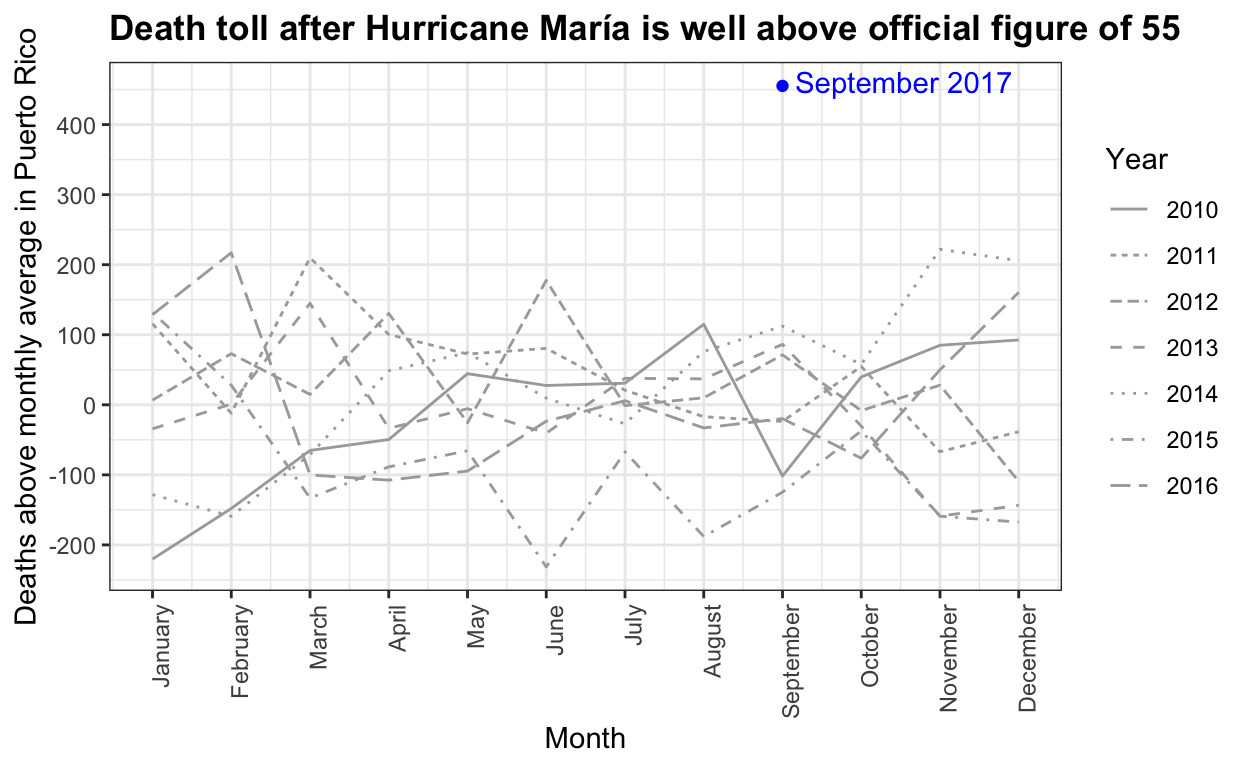

The complex process of obtaining Puerto Rico mortality data: a timeline

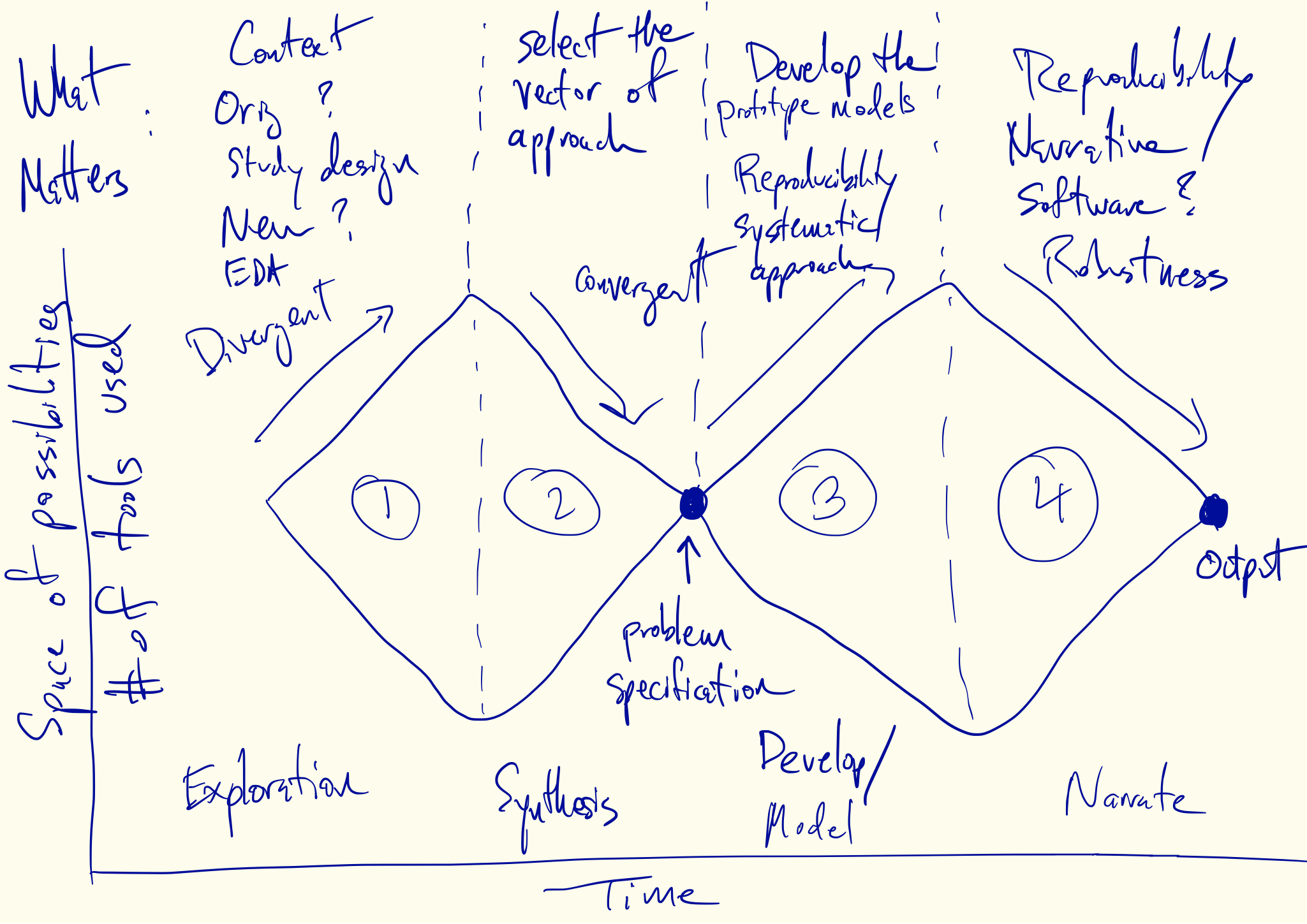

Divergent and Convergent Phases of Data Analysis

Being at the Center

Constructing a Data Analysis

The Law and Order of Data Science

The Trillion Dollar Question

Why I Indent My Code 8 Spaces

Partitioning the Variation in Data

Teaching R to New Users - From tapply to the Tidyverse

What Should be Done When Data Have Creators?

Cultural Differences in Map Data Visualization

Creativity in Data Analysis

The Role of Resources in Data Analysis

People vs. Institutions in Data Analysis

An ode to King James

Estimating mortality rates in Puerto Rico after hurricane María using newly released official death counts

Trustworthy Data Analysis

Context Compatibility in Data Analysis

Awesome postdoc opportunities in computational genomics at JHU

Rethinking Academic Data Sharing

Software as an academic publication

Relationships in Data Analysis

What can we learn from data analysis failures?

Process versus outcome productivity

What is a Successful Data Analysis?

Input on the Draft NIH Strategic Plan for Data Science

What do Fahrenheit, comma separated files, and markdown have in common?

Some datasets for teaching data science

A non-comprehensive list of awesome things other people did in 2017

Thoughts on David Donoho’s "Fifty Years of Data Science"

How Do Machines Learn?

Puerto Rico's governor wants recount of hurricane death toll

Data Analysis and Engagement - Does Caring About the Analysis Matter?

This is a brave post and everyone in statistics should read it

Hurricane María official death count in conflict with mortality data

Some roadblocks to the broad adoption of machine learning and AI

A few things that would reduce stress around reproducibility/replicability in science

Follow Up on Reasoning About Data

Reasoning About Data

How do you convince other people to use R?

It Costs Money to Get It Right

Creating an expository graph for a talk

Recording Podcasts with a Remote Co-Host

Editing Podcasts with Logic Pro X

Specialization and Communication in Data Science

Moon Shots Cost More Than You Think

Deep Dive - Y. Ogata's Residual Analysis for Point Processes

Data Science on a Chromebook

Simple Queue Package for R

Code for my educational gifs

Announcing the tidypvals package

My unfunded HHMI teaching professors proposal

My Podcast Podroll

Optimizing for User Experience

The joy of no more violin plots

The Machines Learn But We Don't

Lowering the GWAS threshold would save millions of dollars

The future of education is plain text

papr - rate papers on biorxiv in a single swipe and help science!

Toward tidy analysis

The Past and Future of Data Analysis

Data on the Comey Effect

Will Machine Learning and AI Ever Solve the Last Mile?

Some default and debt restructuring data

Science really is non-partisan: facts and skepticism annoy everybody

La matrícula, el costo del crédito y las huelgas en la UPR

The Importance of Interactive Data Analysis for Data-Driven Discovery

The levels of data science class

When do we need interpretability?

Model building with time series data

Reproducibility and replicability is a glossy science now so watch out for the hype

My Podcasting Setup

Data Scientists Clashing at Hedge Funds

Not So Standard Deviations Episode 32 - You Have to Reinvent the Wheel a Few Times

Reproducible Research Needs Some Limiting Principles

New class - Data App Prototyping for Public Health and Beyond

User Experience and Value in Products

Got a data app idea? Apply to get it prototyped by the JHU DSL!

Interview with Al Sommer - Effort Report Episode 23

Not So Standard Deviations Episode 30 - Philately and Numismatology

Some things I've found help reduce my stress around science

A non-comprehensive list of awesome things other people did in 2016

The four eras of data

Not So Standard Deviations Episode 28 - Writing is a lot Harder than Just Talking

What is going on with math education in the US?

Not So Standard Deviations Episode 27 - Special Guest Amelia McNamara

Help choose the Leek group color palette

Open letter to my lab: I am not "moving to Canada"

Not all forecasters got it wrong: Nate Silver does it again (again)

Data scientist on a chromebook take two

Not So Standard Deviations Episode 25 - How Exactly Do You Pronounce SQL?

Are Datasets the New Server Rooms?

Distributed Masochism as a Pedagogical Model

Not So Standard Deviations Episode 24 - 50 Minutes of Blathering

Should I make a chatbot or a better FAQ?

The Dangers of Weighting Up a Sample

papr - it's like tinder, but for academic preprints

Information and VC Investing

Not So Standard Deviations Episode 23 - Special Guest Walt Hickey

Statistical vitriol

The Mystery of Palantir Continues

Thinking like a statistician: this is not the election for progressives to vote third party

Facebook and left censoring

Mastering Software Development in R

Not So Standard Deviations Episode 22 - Number 1 Side Project

Interview With a Data Sucker

A Short Guide for Students Interested in a Statistics PhD Program

How to create a free distributed data collection "app" with R and Google Sheets

Not So Standard Deviations Episode 21 - This Might be the Future!

Interview with COPSS award winner Nicolai Meinshausen.

A Simple Explanation for the Replication Crisis in Science

A meta list of what to do at JSM 2016

The relativity of raw data

Not So Standard Deviations Episode 18 - Divide by n-1, or n-2, or Whatever

Tuesday update

Not So Standard Deviations Episode 18 - Back on Planet Earth

A Year at Stack Overflow

Tuesday Update

Ultimate AI battle - Apple vs. Google

Good list of good books

Not So Standard Deviations Episode 17 - Diurnal High Variance

Defining success - Four secrets of a successful data science experiment

Sometimes the biggest challenge is applying what we already know

Sometimes there's friction for a reason

Not So Standard Deviations Episode 16 - The Silicon Valley Episode

Update on Theranos

What is software engineering for data science?

Disseminating reproducible research is fundamentally a language and communication problem

The Real Lesson for Data Science That is Demonstrated by Palantir's Struggles

A means not an end - building a social media presence as a junior scientist

Time Series Analysis in Biomedical Science - What You Really Need to Know

Not So Standard Deviations Episode 15 - Spinning Up Logistics

High school student builds interactive R class for the intimidated with the JHU DSL

An update on Georgia Tech's MOOC-based CS degree

Write papers like a modern scientist (use Overleaf or Google Docs + Paperpile)

As a data analyst the best data repositories are the ones with the least features

Junior scientists - you don't have to publish in open access journals to be an open scientist.

A Natural Curiosity of How Things Work, Even If You're Not Responsible For Them

Not So Standard Deviations Episode 13 - It's Good that Someone is Thinking About Us

Companies are Countries, Academia is Europe

New Feather Format for Data Frames

How to create an AI startup - convince some humans to be your training set

Not So Standard Deviations Episode 12 - The New Bayesian vs. Frequentist

The future of biostatistics

The Evolution of a Data Scientist

Not So Standard Deviations Episode 11 - Start and Stop

Not So Standard Deviations Episode 10 - It's All Counterexamples

Preprints are great, but post publication peer review isn't ready for prime time

Spreadsheets: The Original Analytics Dashboard

Non-tidy data

When it comes to science - its the economy stupid.

Not So Standard Deviations Episode 9 - Spreadsheet Drama

Why I don't use ggplot2

Data handcuffs

Leek group guide to reading scientific papers

A menagerie of messed up data analyses and how to avoid them

Exactly how risky is breathing?

On research parasites and internet mobs - let's try to solve the real problem.

Not So Standard Deviations Episode 8 - Snow Day

Parallel BLAS in R

Profile of Hilary Parker

Not So Standard Deviations Episode 7 - Statistical Royalty

Jeff, Roger and Brian Caffo are doing a Reddit AMA at 3pm EST Today

A non-comprehensive list of awesome things other people did in 2015

Not So Standard Deviations: Episode 6 - Google is the New Fisher

Instead of research on reproducibility, just do reproducible research

By opposing tracking well-meaning educators are hurting disadvantaged kids

Not So Standard Deviations: Episode 5 - IRL Roger is Totally With It

Thinking like a statistician: the importance of investigator-initiated grants

A thanksgiving dplyr Rubik's cube puzzle for you

20 years of Data Science: from Music to Genomics

Some Links Related to Randomized Controlled Trials for Policymaking

Given the history of medicine, why are randomized trials not used for social policy?

So you are getting crushed on the internet? The new normal for academics.

Prediction Markets for Science: What Problem Do They Solve?

Biostatistics: It's not what you think it is

Not So Standard Deviations: Episode 4 - A Gajillion Time Series

How I decide when to trust an R package

Faculty/postdoc job opportunities in genomics across Johns Hopkins

The Statistics Identity Crisis: Am I a Data Scientist

The statistics identity crisis: am I really a data scientist?

Discussion of the Theranos Controversy with Elizabeth Matsui

Not So Standard Deviations: Episode 3 - Gilmore Girls

We need a statistically rigorous and scientifically meaningful definition of replication

Theranos runs head first into the realities of diagnostic testing

Minimal R Package Check List

Profile of Data Scientist Shannon Cebron

Not So Standard Deviations: Episode 2 - We Got it Under 40 Minutes

A glass half full interpretation of the replicability of psychological science

Apple Music's Moment of Truth

We Used Data to Improve our HarvardX Courses: New Versions Start Oct 15

Data Analysis for the Life Sciences - a book completely written in R markdown

The Leek group guide to writing your first paper

Not So Standard Deviations: The Podcast

Interview with COPSS award Winner John Storey

The Next National Library of Medicine Director Can Help Define the Future of Data Science

Interview with Sherri Rose and Laura Hatfield

If you ask different questions you get different answers - one more way science isn't broken it is just really hard

P > 0.05? I can make any p-value statistically significant with adaptive FDR procedures

Correlation is not a measure of reproducibility

UCLA Statistics 2015 Commencement Address

rafalib package now on CRAN

Interested in analyzing images of brains? Get started with open access data.

Statistical Theory is our "Write Once, Run Anywhere"

Autonomous killing machines won't look like the Terminator...and that is why they are so scary

Announcing the JHU Data Science Hackathon 2015

stringsAsFactors: An unauthorized biography

The statistics department Moneyball opportunity

The Mozilla Fellowship for Science

JHU, UMD researchers are getting a really big Big Data center

The Massive Future of Statistics Education

Looks like this R thing might be for real

How Airbnb built a data science team

How public relations and the media are distorting science

Interview at Leanpub

Johns Hopkins Data Science Specialization Captsone 2 Top Performers

Batch effects are everywhere! Deflategate edition

I'm a data scientist - mind if I do surgery on your heart?

Interview with Class Central

Interview with Chris Wiggins, chief data scientist at the New York Times

Science is a calling and a career, here is a career planning guide for students and postdocs

Is it species or is it batch? They are confounded, so we can't know

Residual expertise - or why scientists are amateurs at most of science

The tyranny of the idea in science

Mendelian randomization inspires a randomized trial design for multiple drugs simultaneously

Rafa's citations above replacement in statistics journals is crazy high.

Figuring Out Learning Objectives the Hard Way

Data analysis subcultures

Genomics Case Studies Online Courses Start in Two Weeks (4/27)

Why is there so much university administration? We kind of asked for it.

A blessing of dimensionality often observed in high-dimensional data sets

How to Get Ahead in Academia

Why You Need to Study Statistics

Teaser trailer for the Genomic Data Science Specialization on Coursera

Introduction to Bioconductor HarvardX MOOC starts this Monday March 30

A surprisingly tricky issue when using genomic signatures for personalized medicine

A simple (and fair) way all statistics journals could drive up their impact factor.

Data science done well looks easy - and that is a big problem for data scientists

pi day special: How to use Bioconductor to find empirical evidence in support of pi being a normal number

De-weaponizing reproducibility

The elements of data analytic style - so much for a soft launch

Advanced Statistics for the Life Sciences MOOC Launches Today

Navigating Big Data Careers with a Statistics PhD

Introduction to Linear Models and Matrix Algebra MOOC starts this Monday Feb 16

Is Reproducibility as Effective as Disclosure? Let's Hope Not.

The trouble with evaluating anything

Early data on knowledge units - atoms of statistical education

Johns Hopkins Data Science Specialization Top Performers

Knowledge units - the atoms of statistical education

Precision medicine may never be very precise - but it may be good for public health

Reproducible Research Course Companion

Data as an antidote to aggressive overconfidence

Gorging ourselves on "free" health care: Harvard's dilemma

If you were going to write a paper about the false discovery rate you should have done it in 2002

How to find the science paper behind a headline when the link is missing

Statistics and R for the Life Sciences: New HarvardX course starts January 19

Beast mode parenting as shown by my Fitbit data

Sunday data/statistics link roundup (1/4/15)

Ugh ... so close to one million page views for 2014

On how meetings and conference calls are disruptive to a data scientist

Sunday data/statistics link roundup (12/21/14)

Interview with Emily Oster

Repost: Statistical illiteracy may lead to parents panicking about Autism

A non-comprehensive list of awesome things other people did in 2014

Sunday data/statistics link roundup (12/14/14)

Kobe, data says stop blaming your teammates

Genéticamente, no hay tal cosa como la raza puertorriqueña

Sunday data/statistics link roundup (12/7/14)

Interview with Cole Trapnell of UW Genome Sciences

Repost: A deterministic statistical machine

Thinking Like a Statistician: Social Media and the ‘Spiral of Silence’

HarvardX Biomedical Data Science Open Online Training Curriculum launches on January 19

Data Science Students Predict the Midterm Election Results

Sunday data/statistics link roundup (11/9/14)

Time varying causality in n=1 experiments with applications to newborn care

538 election forecasts made simple

Sunday data/statistics link roundup (11/2/14)

Why I support statisticians and their resistance to hype

Return of the sunday links! (10/26/14)

An interactive visualization to teach about the curse of dimensionality

Vote on simply statistics new logo design

Thinking like a statistician: don't judge a society by its internet comments

Bayes Rule in an animated gif

Creating the field of evidence based data analysis - do people know what a p-value looks like?

Dear Laboratory Scientists: Welcome to My World

I declare the Bayesian vs. Frequentist debate over for data scientists

Data science can't be point and click

The Leek group guide to genomics papers

An economic model for peer review

The Drake index for academics

You think P-values are bad? I say show me the data.

Unbundling the educational package

Applied Statisticians: people want to learn what we do. Let's teach them.

A non-comprehensive list of awesome female data people on Twitter

Why the three biggest positive contributions to reproducible research are the iPython Notebook, knitr, and Galaxy

A (very) brief review of published human subjects research conducted with social media companies

SwiftKey and Johns Hopkins partner for Data Science Specialization Capstone

Interview with COPSS Award winner Martin Wainwright

Crowdsourcing resources for the Johns Hopkins Data Science Specialization

swirl and the little data scientist's predicament

The Leek group guide to giving talks

Stop saying "Scientists discover..." instead say, "Prof. Doe's team discovers..."

It's like Tinder, but for peer review.

If you like A/B testing here are some other Biostatistics ideas you may like

Do we need institutional review boards for human subjects research conducted by big web companies?

Introducing people to R: 14 years and counting

Academic statisticians: there is no shame in developing statistical solutions that solve just one problem

Jan de Leeuw owns the Internet

Piketty in R markdown - we need some help from the crowd

Privacy as a function of sample size

New book on implementing reproducible research

The difference between data hype and data hope

Heads up if you are going to submit to the Journal of the National Cancer Institute

The future of academic publishing is here, it just isn't evenly distributed

What I do when I get a new data set as told through tweets

The Real Reason Reproducible Research is Important

Post-Piketty Lessons

The Big in Big Data relates to importance not size

10 things statistics taught us about big data analysis

Why big data is in trouble: they forgot about applied statistics

JHU Data Science: More is More

Confession: I sometimes enjoy reading the fake journal/conference spam

Picking a (bio)statistics thesis topic for real world impact and transferable skills

Correlation does not imply causation (parental involvement edition)

The #rOpenSci hackathon #ropenhack

Writing good software can have more impact than publishing in high impact journals for genomic statisticians

This is how an important scientific debate is being used to stop EPA regulation

Data Analysis for Genomics edX Course

A non-comprehensive comparison of prominent data science programs on cost and frequency.

The fact that data analysts base their conclusions on data does not mean they ignore experts

The 80/20 rule of statistical methods development

The time traveler's challenge.

ENAR is in Baltimore - Here's What To Do

How to use Bioconductor to find empirical evidence in support of pi being a normal number

Oh no, the Leekasso....

Per capita GDP versus years since women received right to vote

PLoS One, I have an idea for what to do with all your profits: buy hard drives

Data Science is Hard, But So is Talking

Here's why the scientific publishing system can never be "fixed"

Why do we love R so much?

k-means clustering in a GIF

Repost: Ronald Fisher is one of the few scientists with a legit claim to most influential scientist ever

On the scalability of statistical procedures: why the p-value bashers just don't get it.

loess explained in a GIF

Monday data/statistics link roundup (2/10/14)

Just a thought on peer reviewing - I can't help myself.

My Online Course Development Workflow

The three tables for genomics collaborations

Not teaching computing and statistics in our public schools will make upward mobility even harder

Marie Curie says stop hating on quilt plots already.

Announcing the Release of swirl 2.0

The Johns Hopkins Data Science Specialization on Coursera

Sunday data/statistics link roundup (1/19/2014)

Missing not at random data makes some Facebook users feel sad

edge.org asks famous scientists what scientific concept to throw out & they say statistics

Sunday data/statistics link roundup (1/12/2014)

The top 10 predictor takes on the debiased Lasso - still the champ!

Preparing for tenure track job interviews

Sunday data/statistics link roundup (1/5/14)

Repost: Prediction: the Lasso vs. just using the top 10 predictors

The Supreme Court takes on Pollution Source Apportionment...and Realizes It's Hard

Some things R can do you might not be aware of

A non-comprehensive list of awesome things other people did this year.

A summary of the evidence that most published research is false

Sunday data/statistics link roundup (12/15/13)

Simply Statistics Interview with Michael Eisen, Co-Founder of the Public Library of Science (Part 2/2)

Simply Statistics Interview with Michael Eisen, Co-Founder of the Public Library of Science (Part 1/2)

The key word in "Data Science" is not Data, it is Science

Are MOOC's fundamentally flawed? Or is it a problem with statistical literacy?

NYC crime rates by year/commissioner

Advice for students on the academic job market

On the future of the textbook

Academics should not feel guilty for maximizing their potential by leaving their homeland

Sunday data/statistics link roundup (12/2/13)

Statistical zealots

Simply Statistics interview with Daphne Koller, Co-Founder of Coursera

Future of Statistics take home messages. #futureofstats

You must be at least 20 years old for this job

Feeling optimistic after the Future of the Statistical Sciences Workshop

What should statistics do about massive open online courses?

What's the future of inference?

The Leek group guide to sharing data with a data analyst to speed collaboration

Original source code for Apple II DOS

Future of Statistical Sciences Workshop is happening right now #FSSW2013

Survival analysis for hard drives

Apple's Touch ID and a worldwide lesson in sensitivity and specificity

Out with Big Data, in with Hyperdata

How to Host a Conference on Google Hangouts on Air

Sunday data/statistics link roundup (11/3/13)

Unconference on the Future of Statistics (Live Stream) #futureofstats

How to participate in #futureofstats Unconference

Tukey Talks Turkey #futureofstats

Simply Statistics Future of Statistics Speakers - Two Truths, One Lie #futureofstats

Sunday data/statistics link roundup (10/27/13)

(Back to) The Future of Statistical Software #futureofstats

The Leek group guide to reviewing scientific papers

Blog posts that impact real science - software review and GTEX

PubMed commons is launching

Why are the best relievers not used when they are most needed?

Platforms and Integration in Statistical Research (Part 2/2)

The @fivethirtyeight effect - watching @walthickey gain Twitter followers in real time

Platforms and Integration in Statistical Research (Part 1/2)

Teaching least squares to a 5th grader by calibrating a programmable robot

A general audience friendly explanation for why Lars Peter Hansen won the Nobel Prize

Sunday data/statistics link roundup (10/13/13)

Why do we still teach a semester of trigonometry? How about engineering instead?

Cancelled NIH study sections: a subtle, yet disastrous, effect of the government shutdown

The Care and Feeding of Your Scientist Collaborator

The Care and Feeding of the Biostatistician

The Leek group policy for developing sustainable R packages

Sunday data/statistics link roundup (10/6/2013)

Repost: Finding good collaborators

Statistical Ode to Mariano Rivera

Sunday data/statistics link roundup (9/29/13)

Announcing Statistics with Interactive R Learning Software Environment

How could code review discourage code disclosure? Reviewers with motivation.

Is most science false? The titans weigh in.

How I view an academic talk: like a sports game

The limiting reagent for big data is often small, well-curated data

Announcing the Simply Statistics Unconference on the Future of Statistics #futureofstats

Data Analysis in the top 9 courses in lifetime enrollment at Coursera!

So you're moving to Baltimore

Help needed for establishing an ASA statistical genetics and genomics section

Implementing Evidence-based Data Analysis: Treading a New Path for Reproducible Research (Part 3)

Repost: A proposal for a really fast statistics journal

Sunday data/statistics link roundup (9/1/13)

AAAS S&T Fellows for Big Data and Analytics

The return of the stat - Computing for Data Analysis & Data Analysis back on Coursera!

Evidence-based Data Analysis: Treading a New Path for Reproducible Research (Part 2)

Interview with Ani Eloyan and Betsy Ogburn

Statistics meme: Sad p-value bear

Did Faulty Software Shut Down the NASDAQ?

If you are near DC/Baltimore, come see Jeff talk about Coursera

Stratifying PISA scores by poverty rates suggests imitating Finland is not necessarily the way to go for US schools

Chris Lane, U.S. tourism boycotts, and large relative risks on small probabilities

Treading a New Path for Reproducible Research: Part 1

A couple of requests for the @Statistics2013 future of statistics workshop

WANTED: Neuro-quants

Embarrassing typos reveal the dangers of the lonely data analyst

Data scientist is just a sexed up word for statistician

Simply Statistics #JSM2013 Picks for Wednesday

Simply Statistics #JSM2013 Picks for Tuesday

Simply Statistics #JSM2013 Picks for Monday

Sunday data/statistics link roundup (8/4/13)

That causal inference came out of nowhere

The ROC curves of science

The researcher degrees of freedom - recipe tradeoff in data analysis

Sunday data/statistics link roundup (7/28/13)

Statistics takes center stage in the Independent

What are the 5 most influential statistics papers of 2000-2010?

Sunday data/statistics link roundup (7/21/2013)

Defending clinical trials

The "failure" of MOOCs and the ecological fallacy

Name 5 statisticians, now name 5 young statisticians

Yes, Clinical Trials Work

Sunday data/statistics link roundup (7/14/2013)

What are the iconic data graphs of the past 10 years?

Repost: Preventing Errors Through Reproducibility

Use R! 2014 to be at UCLA

Fourth of July data/statistics link roundup (7/4/2013)

Repost: The 5 Most Critical Statistical Concepts

Measuring the importance of data privacy: embarrassment and cost

What is the Best Way to Analyze Data?

Art from Data

Doing Statistical Research

Does fraud depend on my philosophy?

Sunday data/statistics link roundup (6/23/13)

Interview with Miriah Meyer - Microsoft Faculty Fellow and Visualization Expert

Google's brainteasers (that don't work) and Johns Hopkins Biostatistics Data Analysis

Sunday data/statistics link roundup (6/16/13 - Father's day edition!)

The vast majority of statistical analysis is not performed by statisticians

False discovery rate regression (cc NSA's PRISM)

Personalized medicine is primarily a population-health intervention

Why not have a "future of the field" session at a conference with only young speakers?

Sunday data/statistics link roundup (6/2/13)

What statistics should do about big data: problem forward not solution backward

Sunday data/statistics link roundup (5/19/2013)

When does replication reveal fraud?

The bright future of applied statistics

Sunday data/statistics link roundup (5/12/2013, Mother's Day!)

A Shiny web app to find out how much medical procedures cost in your state.

Talking about MOOCs on MPT Direct Connection

Why the current over-pessimism about science is the perfect confirmation bias vehicle and we should proceed rationally

Reproducibility at Nature

Reproducibility and reciprocity

Sunday data/statistics link roundup (4/28/2013)

Mindlessly normalizing genomics data is bad - but ignoring unwanted variability can be worse

Interview at Yale Center for Environmental Law & Policy

Nevins-Potti, Reinhart-Rogoff

Podcast #7: Reinhart, Rogoff, Reproducibility

I wish economists made better plots

Data science only poses a threat to (bio)statistics if we don't adapt

Sunday data/statistics link roundup (4/14/2013)

Great scientist - statistics = lots of failed experiments

Climate Science Day on Capitol Hill

NIH is looking for an Associate Director for Data Science: Statisticians should consider applying

Introducing the healthvis R package - one line D3 graphics with R

An instructor's thoughts on peer-review for data analysis in Coursera

Podcast #6: Data Analysis MOOC Post-mortem

Sunday data/statistics link roundup (3/24/2013)

Youtube should check its checksums

Call for papers for a special issue of Statistical Analysis and Data Mining

Sunday data/statistics link roundup (3/17/13)

Postdoctoral fellow position in reproducible research

Here's my #ENAR2013 Wednesday schedule

If I were at #ENAR2013 today, here's where I'd go

Sunday data/statistics link roundup (3/10/13)

Send me student/postdoc blogs in statistics and computational biology

The importance of simulating the extremes

Big Data - Context = Bad

Sunday data/statistics link roundup (3/3/2013)

Please save the unsolicited R01s

Big data: Giving people what they want

Sunday data/statistics link roundup (2/24/2013)

Tesla vs. NYT: Do the Data Really Tell All?

Sunday data/statistics link roundup (2/17/2013)

Interview with Nick Chamandy, statistician at Google

I'm a young scientist and sequestration will hurt me

Sunday data/statistics link roundup (2/10/2013)

Issues with reproducibility at scale on Coursera

Sunday data/statistics link roundup (2/3/2013)

paste0 is statistical computing's most influential contribution of the 21st century

Data supports claim that if Kobe stops ball hogging the Lakers will win more

Sunday data/statistics link roundup (1/27/2013)

My advanced methods class is now being live-tweeted

Why I disagree with Andrew Gelman's critique of my paper about the rate of false discoveries in the medical literature

Statisticians and computer scientists - if there is no code, there is no paper

Sunday data/statistics link roundup (1/20/2013)

Comparing online and in-class outcomes

R package meme

Review of R Graphics Cookbook by Winston Chang

Welcome to the Smog-ocalypse

Sunday data/statistics link roundup (1/13/2013)

NSF should understand that Statistics is not Mathematics

The landscape of data analysis

By introducing competition open online education will improve teaching at top universities

Sunday data/statistics link roundup (1/6/2013)

Does NIH fund innovative work? Does Nature care about publishing accurate articles?

The scientific reasons it is not helpful to study the Newtown shooter's DNA

Fitbit, why can't I have my data?

Happy 2013: The International Year of Statistics

What makes a good data scientist?

Sunday data/statistics link roundup (12/30/12)

Make a Christmas Tree in R with random ornaments/presents

Sunday data/statistics link roundup 12/23/12

The NIH peer review system is still the best at identifying innovative biomedical investigators

Rafa interviewed about statistical genomics

The value of re-analysis

Should the Cox Proportional Hazards model get the Nobel Prize in Medicine?

Sunday data/statistics link roundup (12/16/12)

Computing for Data Analysis Returns

Joe Blitzstein's free online stat course helps put a critical satellite in orbit

Sunday data/statistics link roundup (12/9/12)

Dropping the Stick in Data Analysis

Email is a to-do list made by other people - can someone make it more efficient?!

Advice for students on the academic job market (2013 edition)

Data analysis acquisition "worst deal ever"?

Sunday data/statistics link roundup (12/2/12)

Statistical illiteracy may lead to parents panicking about Autism.

I give up, I am embracing pie charts

The statisticians at Fox News use classic and novel graphical techniques to lead with data

Sunday data/statistics link roundup (11/25/2012)

Computer scientists discover statistics and find it useful

Developing the New York Times Visual Election Outcome Explorer

A grand experiment in science funding

Podcast #5: Coursera Debrief

Sunday Data/Statistics Link Roundup (11/18/12)

Welcome to Simply Statistics 2.0

Logo Contest Winner

Reproducible Research: With Us or Against Us?

Interview with Tom Louis - New Chief Scientist at the Census Bureau

Some academic thoughts on the poll aggregators

Nate Silver does it again! Will pundits finally accept defeat?

If we truly want to foster collaboration, we need to rethink the "independence" criteria during promotion

Elite education for the masses

Sunday Data/Statistics Link Roundup (11/4/12)

The Year of the MOOC

Microsoft Seeks an Edge in Analyzing Big Data

On weather forecasts, Nate Silver, and the politicization of statistical illiteracy

Computing for Data Analysis (Simply Statistics Edition)

Sunday Data/Statistics Link Roundup (10/28/12)

I love those first discussions about a new research project

Let's make the Joint Statistical Mettings modular

A statistical project bleg (urgent-ish)

Sunday Data/Statistics Link Roundup (10/21/12)

Free Online Education Is Now Illegal in Minnesota

Minnesota clarifies: Free online ed is OK

Simply Statistics Podcast #4: Interview with Rebecca Nugent

Statistics isn't math but statistics can produce math

Making Coffee With R

Comparing Hospitals

A statistician loves the #insurancepoll...now how do we analyze it?

Sunday Data/Statistics Link Roundup (10/14/12)

What's wrong with the predicting h-index paper.

Why we should continue publishing peer-reviewed papers

Fraud in the Scientific Literature

Sunday Data/Statistics Link Roundup (10/7/12)

Not just one statistics interview...John McGready is the Jon Stewart of statistics

Should we stop publishing peer-reviewed papers?

Statistics project ideas for students (part 2)

2-D author lists

This is an awesome paper all students in statistics should read

The more statistics blogs the better

John McGready interviews Jeff Leek

John McGready interviews Roger Peng

Simply statistics logo contest

NBC Unpacks Trove of Data From Olympics

Pro-tips for graduate students (Part 3)

Computing for Data Analysis starts today!

Sunday Data/Statistics Link Roundup (9/23/12)

Prediction contest

Every professor is a startup

In data science - it's the problem, stupid!

Chinese Company to Acquire DNA Sequencing Firm

Online Mentors to Guide Women Into the Sciences

Sunday Data/Statistics Link Roundup (9/16/12)

Statistical analysis suggests the Washington Nationals were wrong to shut down Stephen Strasburg

The statistical method made me lie

An experimental foundation for statistics

Coursera introduces three courses in statistics

The pebbles of academia

Sunday Data/Statistics Link Roundup (9/9/12)

Big Data in Your Blood

The Weatherman Is Not a Moron

Simply Statistics Podcast #3: Interview with Steven Salzberg

Top-down versus bottom-up science: data analysis edition

Simply Statistics Podcast #2

How long should the next podcast be?

Online universities blossom in Asia

Sunday Data/Statistics Link Roundup (9/2/2012)

Drought Extends, Crops Wither

Court Blocks E.P.A. Rule on Cross-State Pollution

Most Americans Confused By Cloud Computing According to National Survey

Court Upholds Rule on Nitrogen Dioxide Emissions

Green: Will Emissions Disclosure Mean Investor Pressure on Polluters?

I.B.M. Mainframe Evolves to Serve the Digital World

Increasing the cost of data analysis

Active in Cloud, Amazon Reshapes Computing

Genes Now Tell Doctors Secrets They Can’t Utter

A deterministic statistical machine

Sunday data/statistics link roundup (8/26/12)

Judge Rules Poker Is A Game Of Skill, Not Luck

Simply Statistics Podcast #1

Science Exchange starts Reproducibility Initiative

Data Startups from Y Combinator Demo Day

Harvard chooses statistician to lead Graduate School of Arts and Sciences

NSF recognizes math and statistics are not the same thing...kind of

Recommended updates from Google Scholar

Interview with C. Titus Brown - Computational biologist and open access champion

Statistics/statisticians need better marketing

Big-Data Investing Gets Its Own Supergroup

Johns Hopkins University Professor Louis Named to Lead Census Bureau Research Directorate

How Big Data Became So Big

Sunday data/statistics link roundup (8/12/12)

When dealing with poop, it's best to just get your hands dirty

Why we are teaching massive open online courses (MOOCs) in R/statistics for Coursera

A non-exhaustive list of things I have failed to accomplish

On the relative importance of mathematical abstraction in graduate statistical education

My worst nightmare...

In which Brian debates abstraction with T-Bone

Samuel Kou wins COPSS Award

If I were at #JSM2012 today, here's where I'd go.

NYC and Columbia to Create Institute for Data Sciences & Engineering

Why I'm Staying in Academia

In Sliding Internet Stocks, Some Hear Echo of 2000

Statistician (@cocteau) to show journalists how it's done

Predictive analytics might not have predicted the Aurora shooter

Tweet up #JSM2012

When Picking a C.E.O. Is More Random Than Wise

Congress to Examine Data Sellers

How important is abstract thinking for graduate students in statistics?

Online education: many academics are missing the point

Smartphones, Big Data Help Fix Boston's Potholes

Voters Say They Are Wary of Ads Made Just for Them

Buy your own analytics startup for $15,000 (at least as of now)

Really Big Objects Coming to R

A Contest for Sequencing Genomes Has Its First Entry in Ion Torrent

I.B.M. Is No Longer a Tech Bellwether (It's too busy doing statistics)

Proof by example and letters of recommendation

Facebook's Real Big Data Problem

Medalball: Moneyball for the olympics

We used, you know, that statistics thingy

Sunday Data/Statistics Link Roundup (7/22/12)

Big Data on Campus

Risks in Big Data Attract Big Law Firms

Interview with Lauren Talbot - Quantitative analyst for the NYC Financial Crime Task Force

Big data is worth nothing without big science

Help me find the good JSM talks

A closer look at data suggests Johns Hopkins is still the #1 US hospital

Johns Hopkins Coursera Statistics Courses

Top Universities Test the Online Appeal of Free

Free Statistics Courses on Coursera

Universities Reshaping Education on the Web

Bits: Betaworks Buys What's Left of Social News Site Digg

Sunday Data/Statistics Link Roundup (7/15/12)

Bits: Mobile App Developers Scoop Up Vast Amounts of Data, Reports Say

GDP Figures in China are for "reference" only

This is Not About Statistics But It is About Emacs

Statistical Reasoning on iTunes U

What is the most important code you write?

How Does the Film Industry Actually Make Money?

My worst (recent) experience with peer review

A Northwest Pipeline to Silicon Valley

Skepticism+Ideas+Grit

The power of power

Replication and validation in -omics studies - just as important as reproducibility

Computing and Sustainability: What Can Be Done?

Meet the Skeptics: Why Some Doubt Biomedical Models - and What it Takes to Win Them Over

Sunday data/statistics link roundup (7/1)

Obamacare is not going to solve the health care crisis, but a new initiative, led by a statistician, may help

Motivating statistical projects

Follow up on "Statistics and the Science Club"

The price of skepticism

Hilary Mason: From Tiny Links, Big Insights

The problem with small big data

A specific suggestion to help recruit/retain women faculty at Hopkins

The Evolution of Music

Sunday data/statistics link roundup (6/24)

Statistics and the Science Club

Pro Tips for Grad Students in Statistics/Biostatistics (Part 2)

E.P.A. Casts New Soot Standard as Easily Met

Pro Tips for Grad Students in Statistics/Biostatistics (Part 1)

Sunday data/statistics link roundup (6/17)

Statisticians, ASA, and Big Data

Big Data Needs May Create Thousands Of Tech Jobs

Green: E.P.A. Soot Rules Expected This Week

Poison gas or...air pollution?

Chris Volinsky knows where you are

Getting a grant...or a startup

Sunday data/statistics link roundup (6/10)

China Asks Embassies to Stop Measuring Air Pollution

How Big Data Gets Real

Interview with Amanda Cox - Graphics Editor at the New York Times

Writing software for someone else

Why "no one reads the statistics literature anymore"

View my Statistics for Genomics lectures on Youtube and ask questions on facebook/twitter

Schlep blindness in statistics

Sunday data/statistics link roundup (5/27)

"How do we evaluate statisticians working in genomics? Why don't they publish in stats journals?" Here is my answer

Sunday data/statistics link roundup (5/20)

Health by numbers: A statistician's challenge

The Numbers Don't Lie

Computational biologist blogger saves computer science department

Facebook Needs to Turn Data Into Investor Gold

Sunday data/statistics link roundup (5/13)

Interview with Hadley Wickham - Developer of ggplot2

What are the products of data analysis?

DealBook: Glaxo to Make Hostile Bid for Human Genome Sciences

Data analysis competition combines statistics with speed

How do you know if someone is great at data analysis?

Illumina stays independent, for now

UCLA Data Fest 2012

Hammer on the importance of statistics

New National Academy of Sciences Members

GE's Billion-Dollar Bet on Big Data

Just like regular communism, dongle communism has failed

Sample mix-ups in datasets from large studies are more common than you think

A disappointing response from @NatureMagazine about folks with statistical skills

Sunday data/statistics link roundup (4/29)

People in positions of power that don't understand statistics are a big problem for genomics

Nature is hiring a data editor...how will they make sense of the data?

How do I know if my figure is too complicated?

On the future of personalized medicine

Sunday data/statistics link roundup (4/22)

Replication, psychology, and big science

Roche: Illumina Is No Apple

Sunday data/statistics link roundup (4/15)

Interview with Drew Conway - Author of "Machine Learning for Hackers"

The Problem with Universities

Statistics is not math...

Evolution, Evolved

Sunday data/statistics link roundup (4/8)

What is a major revision?

Study Says DNA’s Power to Predict Illness Is Limited

Epigenetics: Marked for success

ENAR Meeting

New U.S. Research Will Aim at Flood of Digital Data

R 2.15.0 is released

Big Data Meeting at AAAS

Roche Raises Illumina Bid to $51, Seeking Faster Deal

Justices Send Back Gene Case

R and the little data scientist's predicament

Supreme court vacates ruling on BRCA gene patent!

Some thoughts from Keith Baggerly on the recently released IOM report on translational omics

Sunday data/statistics link roundup (3/25)

This graph shows that President Obama's proposed budget treats the NIH even worse than G.W. Bush - Sign the petition to increase NIH funding!

Big Data for the Rest of Us, in One Start-Up

More commentary on Mayo v. Prometheus

Laws of Nature and the Law of Patents: Supreme Court Rejects Patents for Correlations

Supreme court unanimously rules against personalized medicine patent!

Interview with Amy Heineike - Director of Mathematics at Quid

Sunday data/statistics link roundup (3/18)

Peter Norvig on the "Unreasonable Effectiveness of Data"

A proposal for a really fast statistics journal

Frighteningly Ambitious Startup Ideas

Answers in Medicine Sometimes Lie in Luck

Sunday Data/Statistics Link Roundup (3/11)

Cost of Gene Sequencing Falls, Raising Hopes for Medical Advances

IBM’s Watson Gets Wall Street Job After ‘Jeopardy’ Win

Mission Control, Built for Cities

A plot of my citations in Google Scholar vs. Web of Science

R.A. Fisher is the most influential scientist ever

Are banks being sidelined by retailers' data collection?

Characteristics of my favorite statistics talks

DealBook: Roche Extends Deadline for Illumina Offer

Sunday data/statistics link roundup (3/4)

True Innovation

An essay on why programmers need to learn statistics

Confronting a Law Of Limits

A cool profile of a human rights statistician

Gulf on Open Access to Federally Financed Research

Statistics project ideas for students

The case for open computer programs

Duke Taking New Steps to Safeguard Research Integrity

Graham & Dodd's Security Analysis: Moneyball for...Money

The Duke Saga Starter Set

'WaterBillWoman' pestered city for years over faulty bills

Monitoring Your Health With Mobile Devices

Prediction: the Lasso vs. just using the top 10 predictors

Air Pollution Linked to Heart and Brain Risks

Professional statisticians agree: the knicks should start Steve Novak over Carmelo Anthony

Interracial Couples Who Make the Most Money

Scientists Find New Dangers in Tiny but Pervasive Particles in Air Pollution

60 Lives, 30 Kidneys, All Linked

Company Unveils DNA Sequencing Device Meant to Be Portable, Disposable and Cheap

I don't think it means what ESPN thinks it means

How Companies Learn Your Secrets

I.B.M.: Big Data, Bigger Patterns

A Flat Budget for NIH in 2013 - ScienceInsider

Harvard's Stat 110 is now a course on iTunes

Mathematicians Organize Boycott of a Publisher

Mortimer Spiegelman Award: Call for Nominations. Deadline is April 1, 2012

At MSNBC, a Professor as TV Host

Untitled

The Duke Clinical Trials Saga - What Really Happened

Sunday Data/Statistics Link Roundup (2/12)

The Age of Big Data

Data says Jeremy Lin is for real

Peter Thiel on Peer Review/Science

Duke Saga on 60 Minutes this Sunday

An example of how sending a paper to a statistics journal can get you scooped

DealBook: Illumina Formally Rejects Roche's Takeover Bid

Statisticians and Clinicians: Collaborations Based on Mutual Respect

Wolfram, a Search Engine, Finds Answers Within Itself

An R script for estimating future inflation via the Treasury market

Sunday Data/Statistics Link Roundup (2/5)

Why don't we hear more about Adrian Dantley on ESPN? This graph makes me think he was as good an offensive player as Michael Jordan.

Cleveland's (?) 2001 plan for redefining statistics as "data science"

Evidence-based Music

This graph makes me think Kobe is not that good, he just shoots a lot

Why in-person education isn't dead yet...but a statistician could finish it off

Sunday data/statistics link roundup (1/29)

This simple bar graph clearly demonstrates that the US can easily increase research funding

When should statistics papers be published in Science and Nature?

A wordcloud comparison of the 2011 and 2012 #SOTU

The end of in-class lectures is closer than I thought

Why statisticians should join and launch startups

Sunday Data/Statistics Link Roundup (1/21)

Interview With Joe Blitzstein

Data Journalism Awards

Fundamentals of Engineering Review Question Oops

figshare and don't trust celebrities stating facts

A tribute to one of the most popular methods in statistics

Sunday Data/Statistics Link Roundup

Academics are partly to blame for supporting the closed and expensive access system of publishing

In the era of data what is a fact?

Help us rate health news reporting with citizen-science powered http://www.healthnewsrater.com

Do you own or rent?

Statistical Crime Fighter

A statistician and Apple fanboy buys a Chromebook...and loves it!

Building the Team That Built Watson

Make us a part of your day - add Simply Statistics to your RSS feed

Sunday Data/Statistics Link Roundup

Where do you get your data?

P-values and hypothesis testing get a bad rap - but we sometimes find them useful.

Why all #academics should have professional @twitter accounts

Will Amazon Offer Analytics as a Service?

Baltimore gun offenders and where academics don't live

List of cities/states with open data - help me find more!

Grad students in (bio)statistics - do a postdoc!

An R function to map your Twitter Followers

On Hard and Soft Money

New features on Simply Statistics

In Greece, a statistician faces life in prison for doing his job: calculating and reporting a statistic

Interview with Nathan Yau of FlowingData

Dear editors/associate editors/referees, Please reject my papers quickly

Smoking is a choice, breathing is not.

The Supreme Court's interpretation of statistical correlation may determine the future of personalized medicine

Interview w/ Mario Marazzi, Puerto Rico Institute of Statistics Director, on the importance of Government Statisticians

Plotting BeijingAir Data

Clean Air A 'Luxury' In Beijing's Pollution Zone

Outrage Grows Over Air Pollution and China’s Response

Beijing Air (cont'd)

Who can resist Biostatistics Ryan Gosling?

Online Learning, Personalized

Preventing Errors through Reproducibility

Citizen science makes statistical literacy critical

New S.E.C. Tactics Yield Actions Against Hedge Funds

Reverse scooping

The worlds has changed from analogue to digital and it's time mathematical education makes the change too.

Reproducible Research in Computational Science

Beijing Air

DNA Sequencing Caught in Deluge of Data

Roger's perspective on reproducible research published in Science

Selling the Power of Statistics

Contributions to the R source

Reproducible Research and Turkey

Apple this is ridiculous - you gotta upgrade to upgrade!?

An R function to analyze your Google Scholar Citations page

Data Scientist vs. Statistician

Ozone rules

Show 'em the data!

Interview with Héctor Corrada Bravo

Google Scholar Pages

History of Nonlinear Principal Components Analysis

Amazon EC2 is #42 on Top 500 supercomputer list

OK Cupid data on Infochimps - anybody got $1k for data?

Preparing for tenure track job interviews

First 100 Posts

New O'Reilly book on parallel R computation

The Cost of a U.S. College Education

Cooperation between Referees and Authors Increases Peer Review Accuracy

Expected Salary by Major

Statisticians on Twitter...help me find more!

Coarse PM and measurement error paper

Is Statistics too darn hard?

Reproducible research: Notes from the field

New ways to follow Simply Statistics

Interview with Victoria Stodden

Free access publishing is awesome...but expensive. How do we pay for it?

Guest Post: SMART thoughts on the ADHD 200 Data Analysis Competition

Reproducible Research Talk in Vancouver

We need better marketing

Advice on promotion letters bleg

The 5 Most Critical Statistical Concepts

Computing on the Language

Visualizing Yahoo Email

Archetypal Athletes

Web-scraping

Graduate student data analysis inspired by a high-school teacher

Interview With Chris Barr

The self-assessment trap

Anthropology of the Tribe of Statisticians

Caffo's Theorem

Finding good collaborators

Do we really need applied statistics journals?

Caffo + Ninjas = Awesome

Spectacular Plots Made Entirely in R

Colors in R

Competing through data: Three experts offer their game plan

Where would we be without Dennis Ritchie?